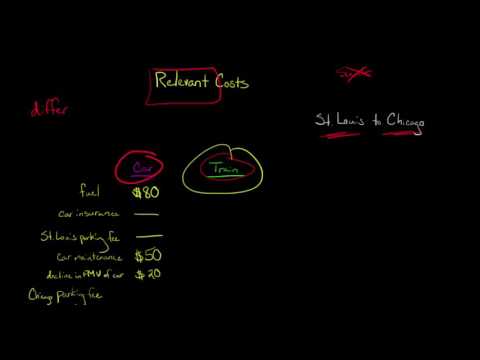

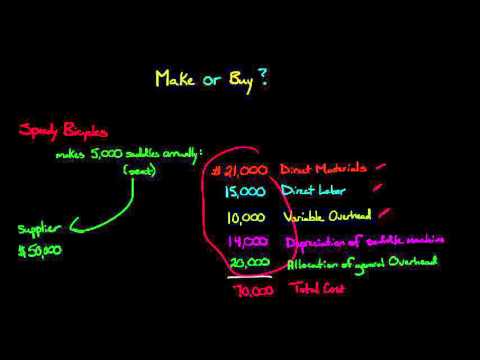

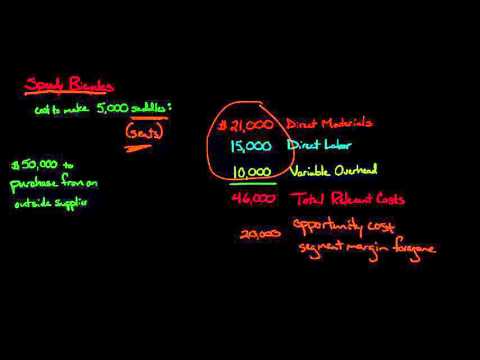

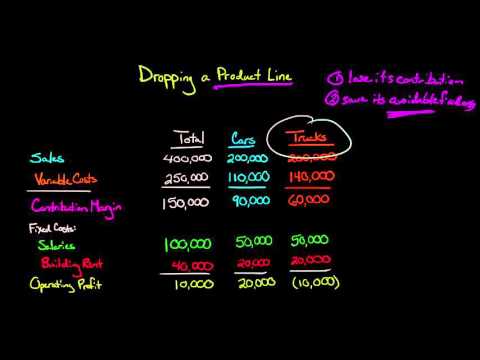

Relevant costs can be defined as any cost relevant to a decision. A matter is relevant if there is a change in cash flow that is caused by the decision. The change in cash flow can be: additional amounts that must be paid. a decrease in amounts that must be paid.What are the two types of relevant costs?

The types of relevant costs are incremental costs, avoidable costs, opportunity costs, etc.; while the types of irrelevant costs are committed costs, sunk costs, non-cash expenses, overhead costs, etc.What is relevant cost and irrelevant cost?

Relevant costs are costs that will be affected by a managerial decision. Irrelevant costs are those that will not change in the future when you make one decision versus another.