Cost accounting is defined as "a systematic set of procedures for recording and reporting measurements of the cost of manufacturing goods and performing services in the aggregate and in detail.What do you mean by cost accounting?

Cost accounting is a method of managerial accounting which aims to capture the total production cost of a business by measuring the variable costs of each production phase as well as fixed costs, such as a lease expense.What are the 4 types of cost?

Following this summary of the different types of costs are some examples of how costs are used in different business applications.

Fixed and Variable Costs.

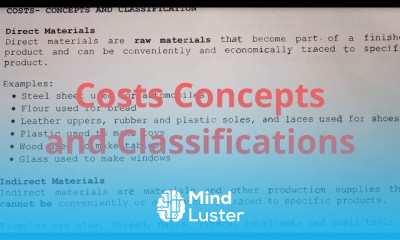

Direct and Indirect Costs. ...

Product and Period Costs. ...

Other Types of Costs. ...

Controllable and Uncontrollable Costs— ...

Out-of-pocket and Sunk Costs—What are the types of cost accounting?

There are four major types of cost accounting: Standard cost accounting, Activity-based cost accounting, Marginal Cost Accounting, Lean Accounting.

Standard Cost Accounting.

Activity-Based Cost Accounting.

Marginal Cost Accounting.

Lean Accounting.What is purpose of cost accounting?

The main objective of cost accounting are ascertainment of cost, fixation of selling price, proper recording and presentation of cost data to management for measuring efficiency and for cost control and cost reduction, ascertaining the profit of each activity, assisting management in decision making process.Who uses cost accounting?

Cost accounting is used by a company's internal management team to identify all variable and fixed costs associated with the production process.What is the difference between cost accounting and financial accounting?

Cost Accounting Records both historical and per-determined costs. Conversely, Financial Accounting records only historical costs. Users of Cost Accounting is limited to internal management of the entity, whereas users of Financial Accounting are internal as well as external parties.